Commentary

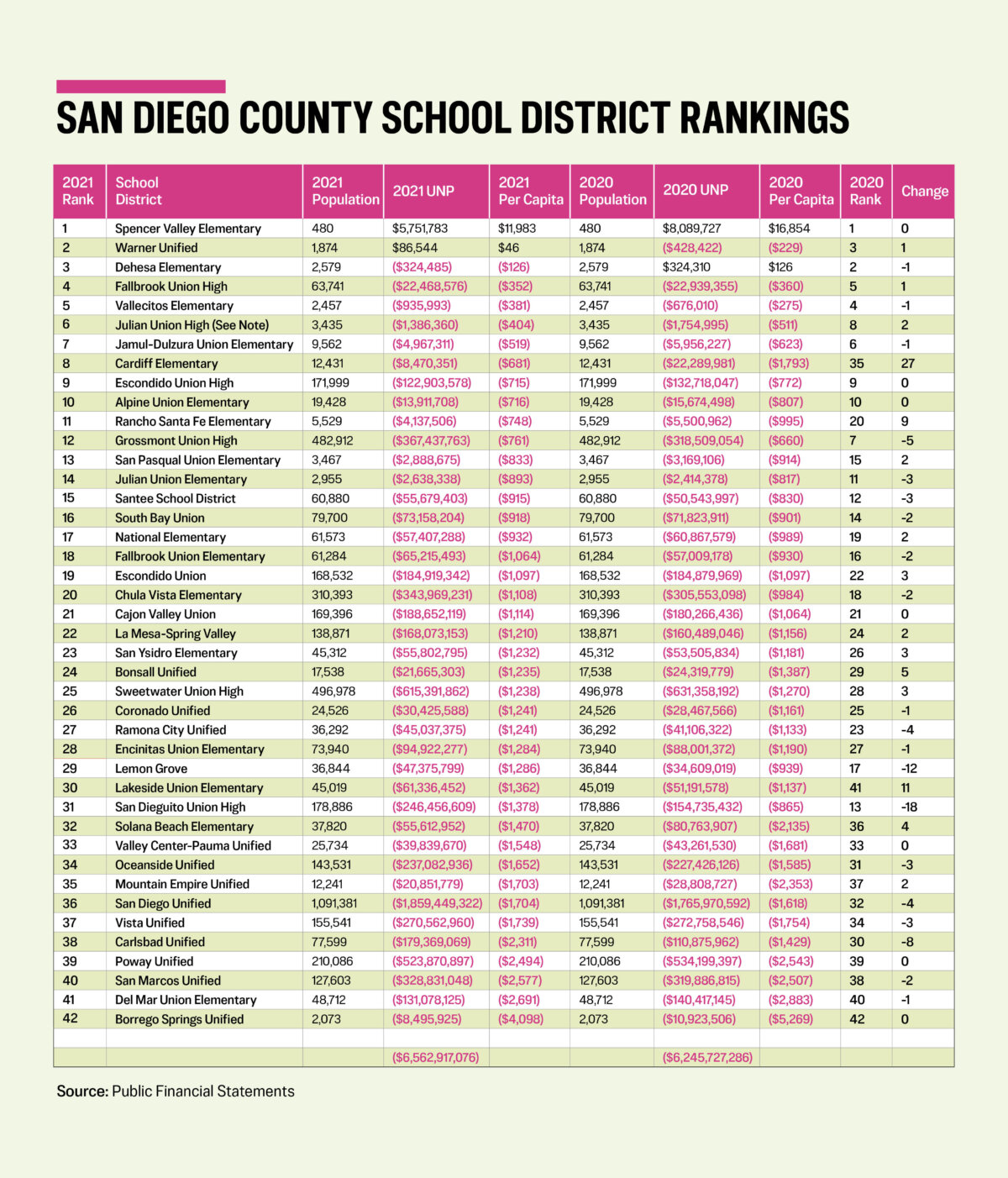

The COVID lockdown year of 2020-2021 was rough on San Diego County’s 42 school districts. Combined, their unrestricted net deficits grew by $319 million.

Taking the unrestricted net position (UNP) for governmental activities for each district, and dividing it by the population they serve, allows for a ranking on a per capita basis.

If you reside in the bottom coastal county in California, the table below provides you with a temperature gauge on how your school district is faring.

With the exception of Borrego Springs Unified, the majority of the 10 districts serving populations of 12,000 residents or less are doing quite well. Three out of every four of the districts pretty much stayed in place. But 11 districts moved four or more positions, warranting a closer look to see why.

The biggest mover was Cardiff Elementary. This small district had revenues in excess of expenditures of $92,104. It also pulled $13,661,725 out of restricted assets and purportedly saw its net investment in capital assets decline by $14,101. The reported impact should have been an increase of $13,819,630 to its unrestricted net deficit. But it was $13,767,930, leaving a difference of $51,700. But the mystery broadens, as the district increased its capital assets by $12,741,878. And there was no increase in related debts.

From an accounting standpoint, things in municipal finance can get really awkward when there is no requirement to provide a disclosure with the financial statement as to how the amount for the “net investment in capital assets” was arrived at. Between the funds transferred out of restricted funds and appropriated for improvements, buildings and equipment, the answer can hopefully be found. The net result finds Cardiff jumping up 27 places in the rankings.

Determining how districts have performed gets interesting when there are two districts in California with the same name. This was the case for Lakeside Union Elementary. In the prior year, 2020, this district dropped 12 places. But using the correct population served, it jumped up 11 positions this year. Meaning that it really didn’t move at all over these two years and that double and triple checking needs to be done by everyone, including me.

Rancho Sante Fe had revenues in excess of expenditures of $2.2 million and transferred $0.6 million of it into restricted assets. It then allocated $0.3 million toward its net investment in capital assets, resulting in a decrease in its unrestricted net deficit of $1.3 million. This activity moved this smaller district up nine places.

Bonsall Unified had revenues in excess of expenditures of $7.5 million and saw depreciation reduce its net investment in capital assets by $1 million. With a transfer of $5.8 million into restricted assets, its unrestricted net deficit was reduced by $2.7 million, moving it up five positions.

Solana Beach had revenues in excess of expenditures of $6.6 million and drew down $21.9 million from restricted assets. It allocated $3.9 million towards net investment in capital assets and had prior period adjustments of $0.07 million, resulting from GASB 84 for fiduciary activities. This Government Accounting Standards Board industry promulgation became effective for fiscal years ending after Dec. 15, 2019. Together it should have reduced its unrestricted net deficit by $25.1 million, but there is a missing $0.57 million. Do a search of the word “adjustment” and you receive 34 hits. Those residing in this district may want a presentation on the difference from its Chief Business Officer. The net result? It moved up four positions.

The largest district, San Diego Unified, dropped four places. It had revenues in excess of expenditures of $126.9 million and a GASB 84 adjustment of $6.7 million. It moved $112.6 million into restricted assets and appropriated $114.5 million for its net investment in capital assets. The result finds that it increased its unrestricted net deficit by $93.5 million.

Ramona Unified had expenditures in excess of revenues of $1.5 million. It also had a decrease in its net investment in capital assets due to depreciation of $0.2 million. Note 16 details that it also had a GASB 84 adjustment. It was for $0.4, due to a “reclassification of student activity funds from agency funds to a special revenue fund.” With a transfer to restricted assets of $2.1 million, its unrestricted net deficit increased by $3.8 million. It also moved down four positions.

Grossmont Union High School District had revenues in excess of expenditures of $31.3 million but transferred $56.4 million into restricted assets and appropriated $27.6 million toward its net investment in capital assets. Combined, its unrestricted net deficit should have increased by $48.9 million, but $3.8 million is unaccounted for. None of the financial statement disclosures on adjustments or prior activities provided the answer. Once again, this is where a schedule detailing the $330.5 million accounting for the district’s net investment in capital assets would have been helpful. The cumulative impact of these activities dropped the district five places.

Carlsbad Unified had revenues in excess of expenditures of $7.4 million and moved a whopping $66.3 into restricted assets. Along with allocating $2.4 million to its net investment in capital assets, its unrestricted net deficit grew by $60.4 million. For some reason, $0.9 million fell off the table and, I repeat myself, better disclosure for the increase in its net investment in capital assets may have clarified the difference. It dropped eight places.

Lemon Grove had revenues in excess of expenditures of $133,676. It transferred $13,543,502 into restricted assets and had depreciation reducing its net investment in capital assets by $244,399. The combination increased its unrestricted net deficit by $13,165,427. Its GASB 84 adjustment of $398,647, explained in Note 15 of the financial statements, explains the difference. The city dropped 12 positions.

San Dieguito Union High dropped 18 places. It had expenditures in excess of income of $5.8 million. It transferred $68.5 million into restricted assets and expended $19.4 million toward its net investment in capital assets. The net result was an increase in its unrestricted net deficit of $91.7 million. Where the missing $2 million went is our last and final mystery. Could it be for a GASB 84 adjustment of the same amount for the inclusion of Associated Student Body funds? Which brings us back to a recurring concern for this fiscal year—being that GASB needs to issue another promulgation for better disclosure.

From a historical perspective, three themes were impacting San Diego’s school districts in the fiscal year ending June 30, 2021: the coronavirus pandemic, the implementation of GASB 84, and the lack of disclosure for net investment in capital assets. The rankings will assist residents in assessing and monitoring their school districts, which is an integral component of their community and their home values.