Commentary

California’s 58 counties enjoyed a relatively calm fiscal year ending June 30, 2023. Even though their official finance directors have the title of auditor-controller, with many of them still being voted in by their county’s electorate, many are still late in providing the audited financial statements in their annual comprehensive financial reports (ACFR). It makes one wonder how their Board of Supervisors can prepare an annual budget without hard fiscal data.

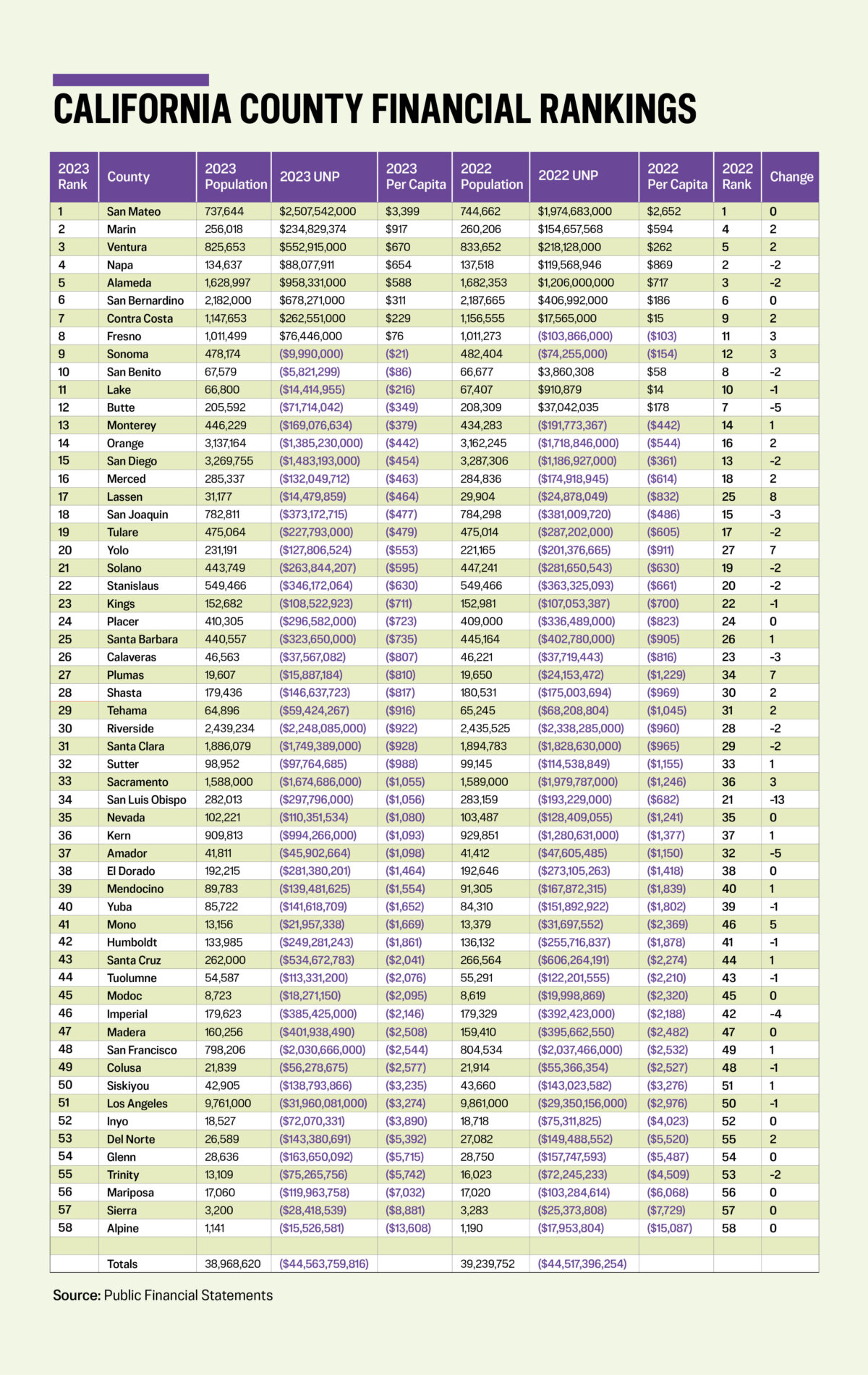

Only 18 counties completed their audits by Dec. 31, 2023, the respected customary due date. Another 22 counties met the March 31, 2024, default deadline. That left 18, or nearly a third, delinquent. Six counties issued them in 2025. Tuolumne County was the last to issue its ACFR for the year ended June 30, 2022 and it is again the last for this year’s 2023 ranking, completing its audit field work on Feb. 27, 2026.

All of California’s counties should have issued their June 30, 2025 ACFRs by now. The California State Association of Auditor-Controllers needs to ask its members to step up their game. Being two years behind is not a good reflection on this professional organization.

What occurred around the state during this time period? And how did your county’s financial status compare to its peers? By taking the unrestricted net position (UNP) for governmental activities, and dividing it by the county’s population, we obtain a per capita that is a simple thermometer of fiscal health.

Eight of the counties moved up or down four positions or more. Going through the graph below, let’s determine the back stories for 10 of them. An overall observation finds that California actually is lowering its population. Another is that the combined unrestricted net positions stayed stable. So, what caused some of the movement?

Lassen County (ACFR completed Sept. 17, 2025) had revenues in excess of expenditures of $14.1 million and transferred $3.9 million into restricted assets, explaining the $10.4 million improvement to its unrestricted net deficit and moving it up eight places.

With Yolo County, let’s clarify one thing. The answer is no, it does not stand for “you only live once.” It’s named after the Patwin Native American term for “a place abounding in rushes.”

I have to admit, as a former audit partner for an accountancy firm during my private sector days, I could not figure out Yolo’s ACFR. It had expenditures in excess of revenues of $1 million, transferred $38 million out of restricted assets and increased its net investment in capital assets by $18.3 million. Combined, this should have increased its unrestricted net deficit by $18.7 million. But the reported increase was $73.6 million.

Management’s discussion starting on page seven didn’t match up to the information in the statement of net position. I can only think that perhaps the report was modified but the changes in the amounts were not updated before the report was released. Amounts for capital assets on page 21 matched up, but not those for longterm liabilities. And this may be where the story lies, because on page 96 one finds that pension liabilities increased by $122.3 million.

A major increase in a liability should have had a similar increase in the unrestricted net deficit. But for Yolo, this amount moved the county up seven places. It did not self-correct in the subsequent year, although this unique accounting did not recur in 2024. Perhaps the 2025 ACFR will provide the needed explanation.

Plumas County had revenues in excess of expenditures of $31.3 million. It transferred $14 million into restricted assets and increased its net investment in capital assets by $9 million. The overall result was a decrease of its unrestricted net deficit of $8.3 million, moving it up seven places.

Must-visit Mono County had revenues in excess of expenditures of $14.9 million. It transferred $2.9 million into restricted assets and spent $3.8 million on its net investment in capital assets, explaining the bulk of its $9.7 million reduction to its unrestricted net deficit and moving up five places.

Shasta County had revenues in excess of expenditures of $54.9 million, transferred $16.7 million into restricted assets and increased its net investment in capital assets by $9.8 million. Combined it explains the $28.4 million reduction in its unrestricted net deficit and its move up three places.

Sacramento County had revenues in excess of expenditures of $497.8 million, transferred $169.8 million into restricted assets and increased its net investment in capital assets by $22.8 million. Combined it explains the $305.2 million reduction in its unrestricted net deficit and its move up three places.

Imperial County provides the anomaly of reducing its unrestricted net deficit, but still losing ground in the rankings, dropping four positions. And it’s all because those in its group, those in the $2,000 per capita unrestricted net deficit range, performed a little better.

Butte County dropped out of the top 10. It had revenues in excess of expenditures of $78.2 million but transferred $162.9 million into restricted assets and $32.2 million into its net investment in capital assets. Combined, this explains the bulk of its unrestricted net position dropping $108.8 million, going from a positive $37 million to a deficit of $71.7 million and dropping five places.

Amador County had revenues in excess of expenditures of $12.9 million and transferred $11.3 million into restricted assets. It actually reduced its unrestricted net deficit by $1.7 million. But several other counties improved their per capitas enough to cause a drop of five places.

San Luis Obispo County had expenditures in excess of revenues of $17 million. It allocated $13 million into net investment in capital assets and transferred $74.6 million into restricted assets. Combined, this explains the increase to its unrestricted net deficit of $104.6 million and its dropping 13 places.

The goal is to move up the rankings. Orange County was in 46th place back in 2010, having been hammered by a $1.7 billion investment loss and the Great Recession. With major modifications to its employee retirement benefit plans 20 years ago, it has moved up to 14th place.

Let’s hope Tuolumne County can complete and release its 2024 audit soon and let the rest of the state see how their counties are doing in a more current and accurate manner.