Insurance premiums are just one piece of the health care affordability puzzle for many Americans. Out-of-pocket expenses, which are less predictable, also affect the family budget.

Those out-of-pocket costs for deductibles, copayments, and the like now average more than $1,600 per year per person. That is on top of insurance premiums, which run to about $27,000 for a family plan.

The Affordable Care Act (ACA)—former President Barack Obama’s health care law, known as Obamacare—aimed to help with both premiums and out-of-pocket costs by providing federal subsidies for low- to middle-class Americans. Subsidies are based on household income as a percentage of the federal poverty level.

There are two kinds of subsidies, one to help with premiums and the other for out-of-pocket spending. Both were intended to be paid directly to insurance companies.

The first subsidies, called advance premium tax credits, reduce premium payments. These are open to individuals making up to about $62,600 per year or families of three making about $107,000.

The second subsidies, called cost-sharing reductions, reduce the copayments, deductibles, and out-of-pocket maximums on certain insurance plans for people making a bit less, up to about $39,000 for an individual or some $66,600 for a family of three.

Together, these subsidies were supposed to make health insurance affordable for people in these income groups.

Yet this plan, like some other provisions of the ACA, had unforeseen consequences because of 16 words from Article 1 of the U.S. Constitution: “No money shall be drawn from the Treasury, but in Consequence of Appropriations made by Law.”

Here is how cost-sharing reductions, which were meant to save money, wound up costing insurers, consumers, and taxpayers even more money than before.

A computer screen shows the enrollment page for the Affordable Care Act in Miami on Nov. 1, 2017. The Affordable Care Act aimed to help with both premiums and out-of-pocket costs by providing federal subsidies for low- to middle-class Americans. (Joe Raedle/Getty Images)

Silver Plans Only

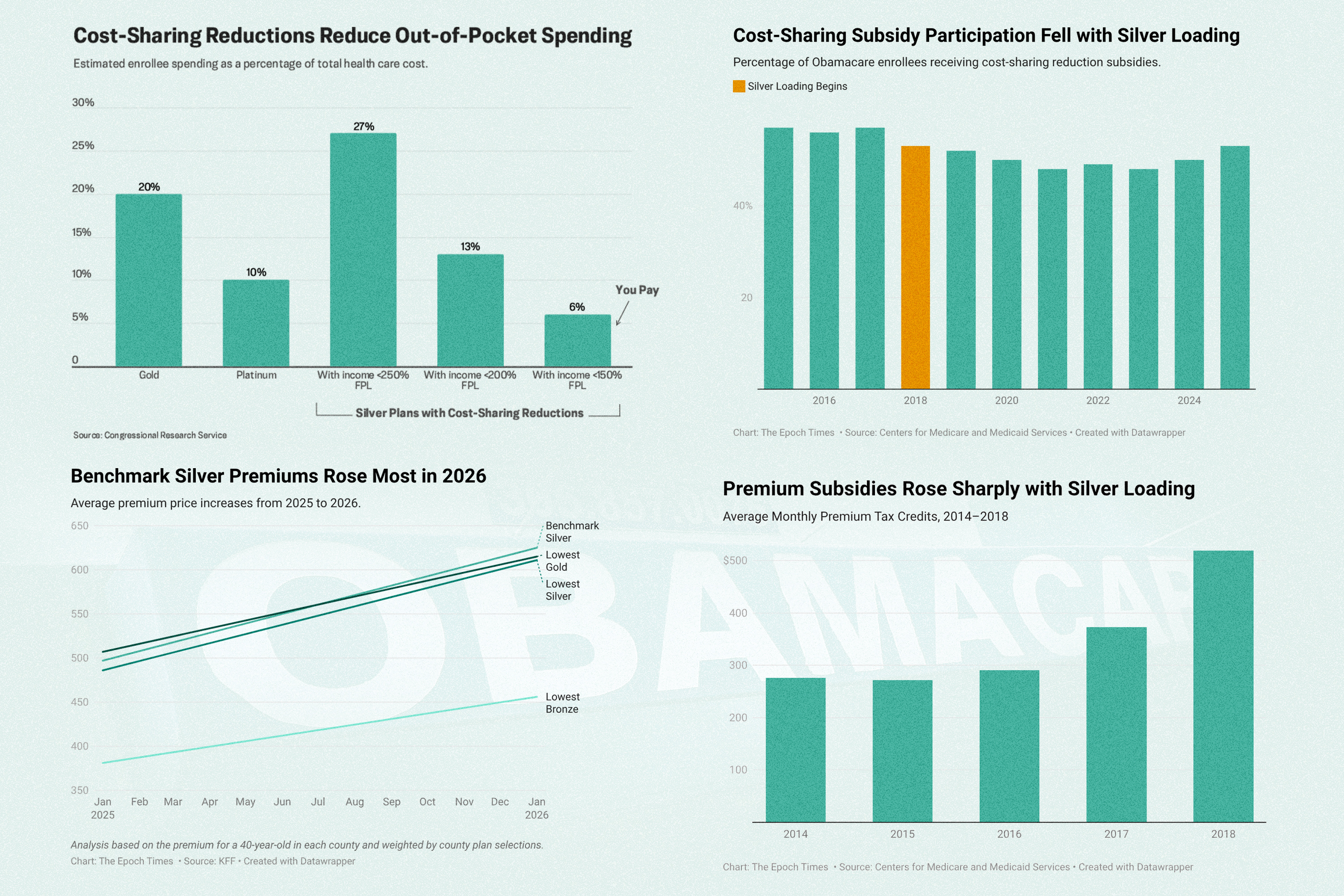

People who qualify for cost-sharing reductions could see their spending on deductibles, copayments, and out-of-pocket maximums reduced by up to 80 percent.

The only catch is that they must select a silver-tier insurance plan to get the benefit.

Obamacare offers four levels of plans: bronze, silver, gold, and platinum. Bronze plans have the lowest premiums, but the deductibles, copayments, and out-of-pocket maximums are higher. Platinum plans have the highest premiums but lower out-of-pocket requirements.

Silver plans are somewhere in the middle and are usually the most popular choice.

On average, customers with a silver plan would pay about 30 percent of their health costs out of pocket, not counting premiums. The insurance company would pay about 70 percent.

With cost-savings reductions, that ratio would change. The insurance company would pick up between 73 percent and 94 percent of the cost, leaving customers to pay as little as 6 percent of provider charges.

For some enrollees, a silver plan could leave them with lower out-of-pocket expenses than even a pricier platinum plan.

Unfunded Payments

Reducing cost-sharing provisions for customers who qualify for them increases costs for insurance companies. So the federal government subsidized the reductions by making additional payments to those insurers. That started with Obamacare in 2014, and those payments grew to more than $5.8 billion in 2017.

But there was a problem.

Although the premium subsidies were added to a list of permanent appropriations, the cost-sharing subsidies were not. That means that for the latter to be funded, Congress has to designate money for them every year, but it has not done so.

An Obamacare logo is shown on the door of the Univista Insurance agency in Miami on Jan. 10, 2017. Since the program started in 2014, federal cost-sharing reduction payments grew to more than $5.8 billion in 2017. (Rhona Wise/AFP via Getty Images)

So in 2016, a federal judge ruled the payments unauthorized but stayed her ruling pending appeal.

Although the ruling was appealed by the Obama administration, in late 2017, the Trump administration stopped the payments, and the appeal was dismissed in May 2018. Congress never appropriated money for the cost-sharing reductions.

Insurers are still obligated by law to reduce the cost-sharing amounts for qualified enrollees in silver plans. But they get no added compensation from the federal government.

Silver Loading, Costs Rising

To cover their added costs, insurers raised premiums on silver plans.

The average premium for benchmark silver plans, the second-lowest priced silver plans, shot up by 34 percent in 2018.

This practice, referred to as silver loading, immediately increased premiums for anyone choosing a silver plan. But the effect was much further reaching.

Benchmark plans are so called because their premium price is used as the benchmark for setting subsidy amounts for all other plans. When the price of benchmark silver plans increased, the federal subsidies for bronze, gold, and platinum plans increased accordingly.

Benchmark silver premiums increased by 17 percent more than bronze premiums did in 2018.

This spike in benchmark premiums inflated subsidies across the Obamacare marketplace, which gave many customers an incentive to choose bronze, or even gold, plans, despite the lure of cost-sharing reductions for silver plans.

“More enrollees could use their premium tax credits to cover most or all of the premium of a bronze tier plan or to reduce their premium contribution for a gold tier plan,” the Government Accountability Office reported in 2024.

For example, 40-year-olds making 200 percent of the federal poverty level could buy a bronze plan in 29 states with a zero dollar premium in 2018, thanks to the increased subsidies, according to a report from the Urban Institute, a Washington-based think tank.

In New Mexico and Pennsylvania, nearly half of such customers could buy a gold plan with a zero dollar premium. In Wyoming, all of them could.

Silver plan enrollments dropped by 11 percentage points in 2018, while bronze plan enrollments grew.

The overall effect increased federal spending by billions of dollars per year.

Even accounting for the savings gained by not paying for cost-sharing reductions, the federal deficit would increase by an estimated $6 billion in 2018, $21 billion in 2020, and $26 billion in 2026, according to a 2017 report from the Congressional Budget Office.

The tax dollars that would have been spent on cost-sharing reductions—and more—now fund increased subsidies to pay for increased premiums for all qualified Obamacare enrollees.

An insurance adviser helps a customer sign up for a health plan under the Affordable Care Act, also known as Obamacare, in Miami on Dec. 15, 2015. (Joe Raedle/Getty Images)

Alternatives

Lawmakers and industry analysts have proposed ways of alleviating the problem, although none have gained widespread acceptance.

One proposal is for Congress to begin appropriating funds for the cost-sharing reduction payments.

Rep. Mariannette Miller-Meeks (R-Iowa) proposed a bill to this effect, which passed the House in December 2025.

Sens. Mike Crapo (R-Idaho) and Bill Cassidy (R-La.) also proposed a bill in December that included appropriations for cost-sharing reductions.

Another plan, proposed by Sen. Roger Marshall (R-Kan.), would provide funded individual health savings accounts to qualified enrollees, which they could use to pay their own out-of-pocket expenses.

“You would use [the health savings account] for your out-of-pocket, your deductibles, and your co-pays,” Marshall said in a Nov. 8, 2025, speech, arguing that the approach would begin to lower premium prices.

Rep. August Pfluger (R-Texas) and Sen. Rick Scott (R-Fla.) introduced a similar plan based on flexible spending accounts.

Democrats, intent on extending Obamacare’s expiring enhanced subsidies, opposed the Republican proposals in the House and Senate.

U.S. Senate Minority Leader Chuck Schumer (D-N.Y.) speaks to reporters following a Senate Democratic policy luncheon at the U.S. Capitol on Dec. 9, 2025. Democrats are pushing to extend the Affordable Care Act’s enhanced subsidies. (Heather Diehl/Getty Images)

“Their phony proposal is dead on arrival,” Senate Minority Leader Chuck Schumer (D-N.Y.) said on Dec. 9, 2025, calling it “junk insurance.”

“The Crapo/Cassidy bill would not extend the [ACA] tax credits for a single day,” Schumer said.

Premium prices increased significantly for all Obamacare plans for 2026, driven in part by insurers’ reaction to the expiration of the enhanced subsidies.

Premiums for benchmark silver plans went up by the most.

Correction: A previous version of this article misstated the nature of a federal judge’s stay of a ruling on Affordable Care Act cost-sharing reduction payments and the date that an appeal of that decision was dismissed. The Epoch Times regrets the errors.