China has just wrapped up its Two Sessions, its biggest political meeting of the year, with Beijing setting a 2026 growth target of 4.5 percent to 5 percent—the country’s lowest target since 1991.

For years, Beijing has set steady growth targets to project stability. Analysts told The Epoch Times that the lower expectations point to a deeper problem: The economy may be much weaker than headline gross domestic product (GDP) numbers suggest.

The warning signs, analysts said, are already visible in the data the regime cannot easily adjust: falling tax revenue, another sharp drop in land-sale income, a prolonged property slump, weak private investment, soft consumer demand, and more figures that Beijing has changed, delayed, or stopped publishing altogether.

“When Beijing cut its 2026 growth target to 4.5 [percent] to 5 percent, it did more than lower expectations,” U.S.-based Chinese economist Li Hengqing told The Epoch Times. “It was making a quiet admission that China’s slowdown is no longer a temporary soft patch that can be covered by one neat GDP number.”

The better way to read China’s economy, Li said, is to ask not whether every official number is true or false, but which numbers are hardest to smooth over.

By that measure, he said, the picture is grim.

Tune in to China Watch, a podcast on Chinese politics, technology, and business.

A Lower Target and a Bigger Signal

Economists and analysts have long doubted the reliability of China’s headline GDP data. Those doubts have intensified in recent years, as visible strains in the economy clash with growth figures that repeatedly land right on target.

Official figures put GDP growth at 5 percent in both 2024 and 2025, hitting Beijing’s target exactly. However, some outside estimates suggest that the regime may have overstated growth by 2 to 3 percentage points.

The Rhodium Group, a New York City-based think tank, estimated China’s real GDP growth in 2025 at about 2.5 percent to 3 percent, with a forecasted growth of 1 percent to 2.5 percent for 2026. Swiss banking group UBS estimated 3.4 percent growth for 2025 and 3 percent for 2026.

A worker sweeps the road next to a billboard reading “Beijing” in the Central Business District in Beijing on Oct. 18, 2024. Beijing set a 2026 gross domestic product growth target of 4.5 percent to 5 percent—the country’s lowest since 1991. (Kevin Frayer/Getty Images)

The International Monetary Fund (IMF) said the country’s private domestic demand remained weak, headline inflation averaged zero, and the GDP deflator—a broad measure of prices across the economy—continued to decline.

Growth, the IMF said, was supported mainly by exports and policy stimulus.

Chinese officials openly called the insufficient domestic demand a “major issue” and urged action.

“The mismatch is hard to ignore,” Li said, noting that these discrepancies do not line up with a clean 5 percent growth rate.

Gao Shanwen, a prominent economist at the Chinese state-owned SDIC Securities, said at a December 2024 conference in Washington that China’s GDP growth “probably averaged around 2 percent” in the past two to three years even though the official number hovered near 5 percent.

“We do not know the true number of China’s real growth figure and maybe some other numbers,” he said.

Harder-to-Hide Numbers

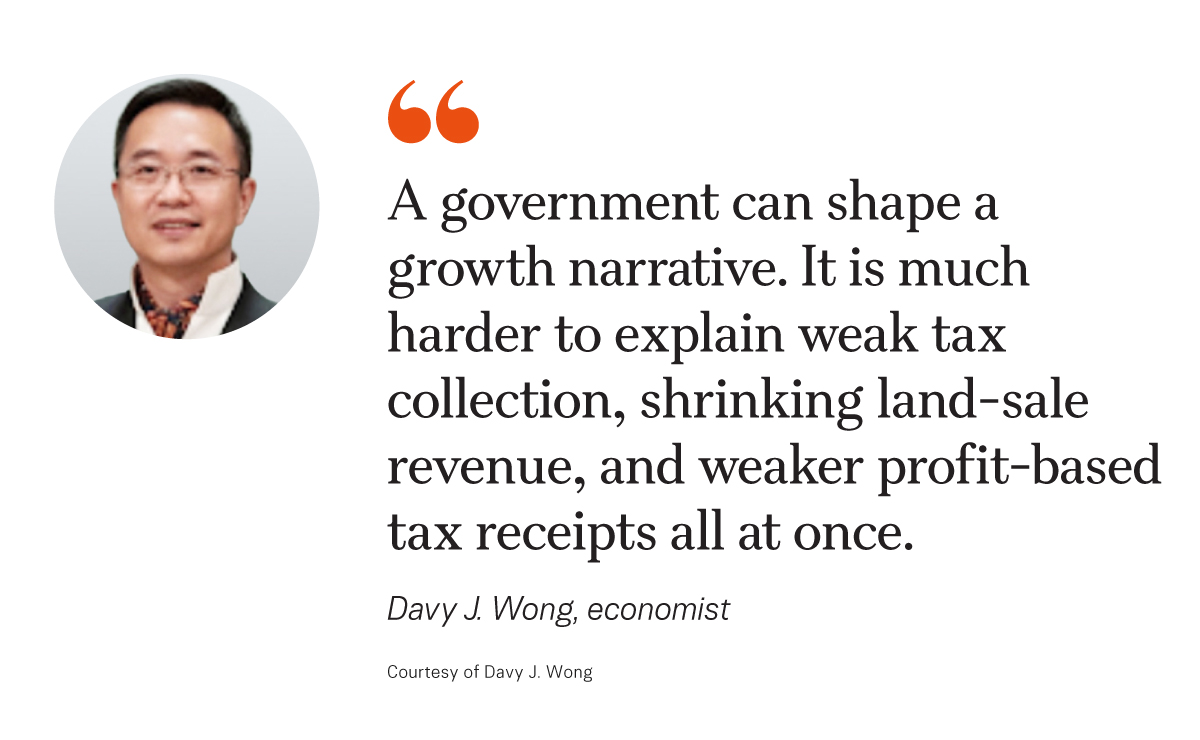

The more telling signals are not in the headline growth rate but in the money actually moving through the system, U.S.-based economist Davy J. Wong told The Epoch Times.

China’s general public budget revenue fell by 1.7 percent in 2025. Local governments’ land-sale income—a major source of cash for local authorities—dropped by another 14.7 percent, marking the fourth straight annual decline. Additionally, the World Bank Group found that overall fiscal revenue remained subdued and corporate income tax receipts fell by 3.1 percent as profit margins narrowed.

“A government can shape a growth narrative,” Wong said. “It is much harder to explain weak tax collection, shrinking land-sale revenue, and weaker profit-based tax receipts all at once.”

Similar weakness can be seen across the private economy.

Investment in fixed assets, such as buildings and equipment, fell by 3.8 percent in 2025, while private investment dropped by 6.4 percent, according to China’s National Bureau of Statistics.

Commuters walk by new office towers under construction as they head to work in the Central Business District in Beijing on Oct. 18, 2024. Investment in fixed assets such as buildings and equipment fell by 3.8 percent in 2025, while private investment dropped by 6.4 percent. (Kevin Frayer/Getty Images)

Month-to-month data show the same pattern. The bureau’s seasonally adjusted fixed-asset investment series was negative for every month of 2025. Retail sales also declined month over month in June, July, September, November, and December. In April 2025, the state injected 520 billion yuan (about $75 billion) into four large banks as part of a stimulus package announced in 2024.

“That is a striking move for an economy that is supposed to be steadily expanding at 5 percent,” Li said.

Wong said these numbers do not reflect a recovery spreading across the domestic economy.

“It looks more like an economy being held up by selected sectors, state support, and exports, while the private economy stays weak underneath,” he said.

The World Bank Group reached a similar conclusion in its assessment of Beijing’s stimulus efforts. It estimated a fiscal push of about 1.6 percent of GDP in 2025 but said only about 0.5 percent went directly to households, with most support still flowing through public investment.

Its report also states that private credit demand remained weak despite easier monetary policy. Households were held back by slower income growth, falling home prices, and debt equal to 139 percent of disposable income.

Beijing’s own language has also undercut its headline numbers. Chinese leader Xi Jinping has called for faster action to address weak domestic demand, especially consumption. Another senior official said expanding domestic demand will be the top priority in 2026.

At the same time, regulators have pledged to tackle the “involution-style” competition and “disorderly price wars” in sectors such as autos.

People attend the 20th Shanghai International Automobile Industry Exhibition in Shanghai on April 19, 2023. State regulators have pledged to tackle the “involution-style” competition and “disorderly price wars” in sectors such as autos. (Hector Retamal/AFP via Getty Images)

Involution-style competition refers to cutthroat rivalry in which firms chase limited demand through price cuts, overproduction, and imitation—eroding profits without creating real gains.

“Strip away the slogans and the message is clear,” Li said. “Firms are cutting prices too hard, households are not spending enough, and the leadership knows growth is too dependent on supply.”

China’s downward demographic trend adds further pressure. The population fell by 3.39 million in 2025, with 7.92 million births and 11.31 million deaths.

A shrinking population does not cause a slowdown overnight, but it makes adjustment much harder in an economy already struggling with debt, weak demand, and falling confidence, Wong said.

The Property Slump

The property market remains one of the biggest drags on China’s growth.

In 2025, real estate investment fell by 17.2 percent. New housing starts dropped by 20.4 percent, while sales by value declined by 12.6 percent. Developers’ funding also fell by 13.4 percent, including a 17.8 percent drop in mortgage-related funds, according to China’s National Bureau of Statistics. By December, all 70 large and medium-sized cities tracked by the bureau were still recording month-to-month declines in secondhand home prices.

Sun Kuo-Hsiang, an international affairs professor at Taiwan’s Nanhua University, told The Epoch Times that these figures represent an ongoing slump that continues to drain local government finances, household wealth, and confidence.

The trends in the housing market are deeply tied to China’s broader economy. During the boom years, developers bought land from local governments at high prices, providing a major source of revenue and signaling future construction.

That model began to break down in 2020, when regulators introduced the “three red lines” policy to limit developers’ leverage by capping debt relative to cash, equity, and assets. The shift helped trigger the default and liquidation of Evergrande, once China’s largest property developer, and deepened the broader downturn.

A salesperson standing next to a housing estate model at a property sales center in Tianjin, China, on June 5, 2024. China’s property market remains a major drag on growth, with all 70 large and medium-sized cities tracked by the National Bureau of Statistics still recording monthly declines in secondhand home prices as of December 2025. (Jade Gao/AFP via Getty Images)

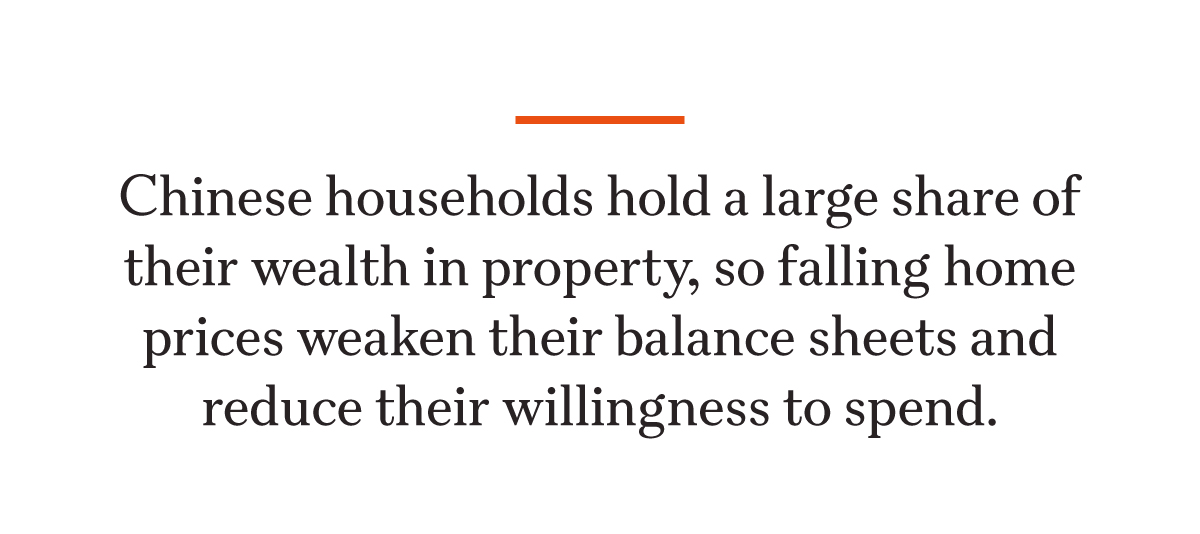

The credit stress that followed in 2021 is still working its way through the sector. Research by Harvard economist Kenneth Rogoff and IMF economist Yang Yuanchen estimates that real estate and its supply chain—construction materials, home furnishings, and related services—account for roughly one-quarter to one-third of China’s GDP.

When home prices fall and construction slows, the effects spread across the economy—from steel and cement to appliances, real estate brokers, and service jobs.

The impact is also direct. Chinese households hold a large share of their wealth in property, so falling home prices weaken their balance sheets and reduce their willingness to spend.

The property downturn has also made some data more sensitive. China does not publish an official housing vacancy rate, and analysts have long tried to assess how much developers overbuilt.

In 2022, the Beike Research Institute, a Chinese think tank, released a report showing that the average housing vacancy rate across 28 Chinese cities was higher than in the United States, Canada, France, and the UK, pointing to oversupply. The report drew attention because of the lack of official data.

A few days later, Beike withdrew the report and apologized, saying that some of the data were inaccurate. Sun suggested that the report was pulled because of pressure from Beijing.

The Missing Data Problem

Since at least 2022, Chinese authorities have stopped publishing hundreds of data series once used by researchers and investors, including figures on land sales, foreign investment, unemployment, housing vacancies, cremations, business confidence, soy sauce production, and vaccination data.

In most cases, authorities have not explained why the data were removed or withheld.

Job seekers attend a job fair in Beijing on March 20, 2024. In June 2023, China’s official youth unemployment rate reached a record 21.3 percent. (Jade Gao/AFP via Getty Images)

The missing figures often relate to politically sensitive areas, especially housing. The shift comes as the property downturn has wiped out billions of dollars in household wealth and triggered protests from frustrated homebuyers.

The handling of youth unemployment is another example of missing figures.

In June 2023, China’s official youth unemployment rate reached a record 21.3 percent. At about the same time, Peking University economist and professor Zhang Dandan drew national attention after saying that the real rate could be as high as 46.5 percent.

In August that year, authorities said they would suspend publication of youth unemployment data, citing the need to revise how it was calculated. Five months later, Beijing released a new series, putting the youth jobless rate at 14.9 percent.

Officials said the revised figure excluded nearly 62 million full-time university students, arguing that they should not be counted as unemployed. But Wong noted that standard statistical practice typically includes anyone actively seeking work, including students.

For comparison, the Organization for Economic Cooperation and Development’s youth unemployment average stood at 11.2 percent in July 2025, with the United States at 10.8 percent and Japan at 4.1 percent.

Why There’s Doubt About Official Numbers

In 2007, former Chinese Premier Li Keqiang famously told the U.S. ambassador that GDP figures from a province he governed were “man-made” and therefore unreliable, according to a leaked U.S. diplomatic cable. Instead, he said, he relied on electricity use, rail freight, and new bank lending to judge real activity.

Chinese Premier Li Keqiang answers questions during a news conference following the closing session of the National People’s Congress in Beijing on March 15, 2015. In 2007, he famously told the U.S. ambassador that gross domestic product figures from a province he governed were “man-made” and unreliable, according to a leaked U.S. diplomatic cable. (Feng Li/Getty Images)

Official GDP figures were “for reference only,” the then-premier reportedly said.

Wong said the remark captured the core problem in China’s statistical system: The numbers often serve a political purpose.

“In China, statistics are not just a technical issue,” Wong said. “They are also a bureaucratic incentive issue, and at the same time a political task handed down by the central authorities as part of maintaining governing legitimacy.”

Local officials have strong reasons to make the numbers look better, he said, because economic performance has long been tied to political evaluation, promotion, and accountability.

When Beijing sets clear goals for growth, employment, and stability, the safest move for local authorities is often not to report the full extent of the problem but to push the figures into an “acceptable range,” Wong said.

That helps explain why analysts are skeptical when official growth lands exactly on target, he said. China’s reported GDP growth of 5 percent in 2024 matched the government’s target precisely.

“Before the year even begins, they’ve already ‘accurately predicted’ their full-year economic performance,” Li Hengqing said.

“This is something virtually unheard of anywhere else in the world—truly unique,” he said.

“Economic growth is something that must be produced in reality; it isn’t something you can simply fabricate or write into existence. But in China, that distinction doesn’t really exist. These numbers are, in essence, manufactured.”

Kang Yi, director of the National Bureau of Statistics, speaks during a news conference about the national economic performance for 2024 in Beijing on Jan. 17, 2025. (Adek Berry/AFP via Getty Images)

He said he has seen how the process works.

“Data originates at the grassroots level—townships report to counties, counties to cities, cities to provinces, and finally to the National Bureau of Statistics,” he said.

At the lowest level, companies report output and revenue but are told that the figures are not tied to taxes, so they feel safe inflating them.

If the numbers fall short of targets—such as the State Council’s 5 percent growth goal—they are sent back for “rechecking,” which in practice means revising them upward, Li Hengqing said.

“Everyone understands the game: Adjust the numbers until they meet expectations,” he said.

That process, according to him, inflates the figures layer by layer all the way up the chain.

He also pointed to past cases in which provinces admitted to major distortions. Inner Mongolia, for example, admitted in 2018 that it had inflated fiscal and industrial data by up to 40 percent. Liaoning Province, meanwhile, acknowledged in 2017 that it had overstated its economic figures by more than 20 percent.

Reuters and Gu Xiaohua contributed to this report.