The concept of someday owning a home and being free of the costly burden of renting seems impossible for 27-year-old Harrison in Fargo, North Dakota.

Although he has a budget ceiling of $350,000 and $30,000 in cash for a down payment and closing costs, the median home listing price for his midwestern city towers at $389,500, according to Realtor.com data.

With the added expense of property taxes and home insurance premiums, Harrison, who asked to remain anonymous because of potential repercussions to his career, said he is worried that he’ll never be able to afford a home—even with a paid-off car, zero credit card debt, and no student loans.

“I am not picky when it comes to homes since I don’t have a family,” he told The Epoch Times. “All I’m looking for is a home with a good foundation and in a safe neighborhood.”

Harrison is not alone: Millennials, born in 1981 to 1996, and others like him in Generation Z, born in 1997 to 2012, face an uphill battle on the path to first-time home ownership, particularly in the years following the COVID-19 pandemic.

While the reasons for home unattainability vary, factors include historically high prices, three years of stubborn inflation and higher interest rates, personal debt and spending habits, unemployment, property scarcity, and wages.

Other millennials and Gen Zers who spoke with The Epoch Times pointed to massive increases in sale prices on homes that were considered affordable 30 years ago.

Some have turned to clever solutions to break into the home market.

Daniel McDonald, 30, teaches house hacking techniques to other young homebuyers. (Courtesy of Daniel McDonald)

Daniel McDonald, 30, became the winning bidder on a 1,600-square-foot, two-bedroom, two-bathroom duplex in Beverly, Massachusetts, after the original buyer backed out at the beginning of the COVID-19 pandemic when prices were relatively low.

He rented out part of the property, saved the proceeds, and bought another duplex a few streets away in 2022.

Yet despite his success with a practice known as “house hacking”—when you generate passive income from a piece of a property while residing there—Mr. McDonald told The Epoch Times that it could be 10 years or longer before he and his wife can afford a single-family home in their area.

Currently, the lowest price home for sale in Beverly on home marketplace Zillow is a three-bedroom, one-bathroom house for $565,000, after a $15,000 price cut on July 2.

A real estate agent (L) shows a couple a home for sale in Cutler Bay, Fla., on April 20, 2023. (Joe Raedle/Getty Images)

“If we moved to a single-family [house] right now and bought that, we’d be spending $4,000 or $5,000 a month [on mortgage payments] with no help. It’s not like it’s an easy option,” he said, adding that limited inventory in the area is also a factor.

David Adams, 37, founded Sniffspot to pair homeowners who have yards and outdoor spaces with pet owners in apartments and condominiums. (Courtesy of David Adams)

In Seattle, David Adams, 37, was racked with student debt and living in a high-rise apartment when he started Sniffspot, a business that allows homeowners to earn passive income while residing in their homes by renting out their yards and outdoor spaces to pet owners who live in apartments and condominiums.

Mr. Adams was looking for a home to accommodate his dogs when he bought a house in Salem, Massachusetts, during the COVID-19 pandemic when interest rates were lower and prices competitive. Still, with student debt to pay off and only self-employment income from his business, qualifying for a home wasn’t easy.

“It’s hard to find an affordable home in general and much harder to find an affordable home that provides a great life for dogs,” he told The Epoch Times.

Mr. Adams said that in a time of high inflation and sluggish wages, many of his clients are using their Sniffspot proceeds to “cover their mortgage and real estate taxes.”

Stephanie Douglass, 35, and Kristina Modares, 34, took an innovative approach to make buying a home affordable for them: They found friends to pool resources to purchase and co-own their first homes in Austin, Texas, in 2013 and 2015, respectively.

Finding success, they decided to teach the approach to others by founding Open House Austin in 2019 and later Open House Education to expand their process to a nationwide audience.

Even with their success, they say the market is much different today than it was 10 years ago.

“Now, it’s not only expensive, but the home prices are high, and [so are] the interest rates,” Ms. Modares told The Epoch Times.

Ms. Douglass said millennials and Gen Zers are facing new obstacles compared with those of homebuyers decades ago.

“It’s a very different market and world that first-time homebuyers are in now than when their parents were trying to do this,” she told The Epoch Times, adding that many young people are gig or freelance workers without the same income history.

“So there’s just a lot of factors changing in the world, and real estate is like an old industry and is not catching up as quickly as the world’s moving,” Ms. Douglass said.

Kristina Modares, 34, (L) and Stephanie Douglass, 35, teach young buyers how to afford homes with their businesses, Open House Austin and Open House Education. (Courtesy of Open House Austin)

Home Prices Soar

Home prices in the United States hit a new high in June, with the median home sale price climbing to $394,000—a 4.4 percent year-over-year increase, according to Redfin.The average homebuyer’s monthly housing payment is $2,829. That’s $30 less than the record high in April, but it’s more than double what it was three years ago. In 2021, the median monthly mortgage payment was $1,242, compared with $972 in 2011, according to Bankrate.

Using economic data on historical home prices and household incomes from the Federal Reserve, a Visual Capitalist report illustrates how, in 1984, the house sale price-to-income ratio was at 3.49 as the median annual household income for Americans was $22,420 and the median house sale price was $78,2000.

That ratio climbed to 5.8 in 2022 as the median household income rose to $74,580 and the median house sale price skyrocketed to $442,600 in quarter four. The ratio, however, dropped to 4.9 in 2023, according to a 2024 Harvard report.

The study authors noted that despite the decrease, “it nonetheless means that homeownership is unaffordable to many households.”

While Federal Reserve data indicate that between 1971 and 2024, the current 6.86 percent rate for a 30-year fixed rate mortgage has stayed below the historic highs of 18 percent or more seen in the early 1980s, interest rates soared after hitting historic lows of 2.65 percent in January 2021. This was because of the Fed’s raising interest rates to combat inflation, which significantly increased mortgage rates on homes.

Mortgage down payments are also high. Zillow released a June 20 study that found that for a “typical” U.S. home valued at roughly $360,000, homebuyers with a median income would need to put down nearly $127,750 to secure a mortgage that would ensure monthly payments were 30 percent or less of their monthly income.

Zillow noted that five years ago, when mortgage rates were just above 4 percent and many home values were roughly half as much as they are now, a similar home would have been affordable with no money down.

Homes near the Chesapeake Bay in Centreville, Md., on March 4, 2024. (Jim Watson/AFP via Getty Images)

Inflation and Unemployment

The annual inflation rate in June 2022 climbed to 9.1 percent in the largest increase in 40 years. While the inflation rate has gradually come down since then, the current rate of 3.3 percent is still significantly higher than the average 0.1 percent seen in 2015.Even though median household incomes have increased more slowly than home prices have, a 2024 analysis from the Federal Reserve Bank of New York shows that wealth for Americans ages 18 to 39 far outpaced that of other age groups in the post-COVID-19 pandemic years, increasing by 80 percent compared with by 10 percent for those ages 40 to 54, and by 30 percent for those ages 55 and older.

The disparity is attributed to rapid increases in the value of financial assets for those younger than 39.

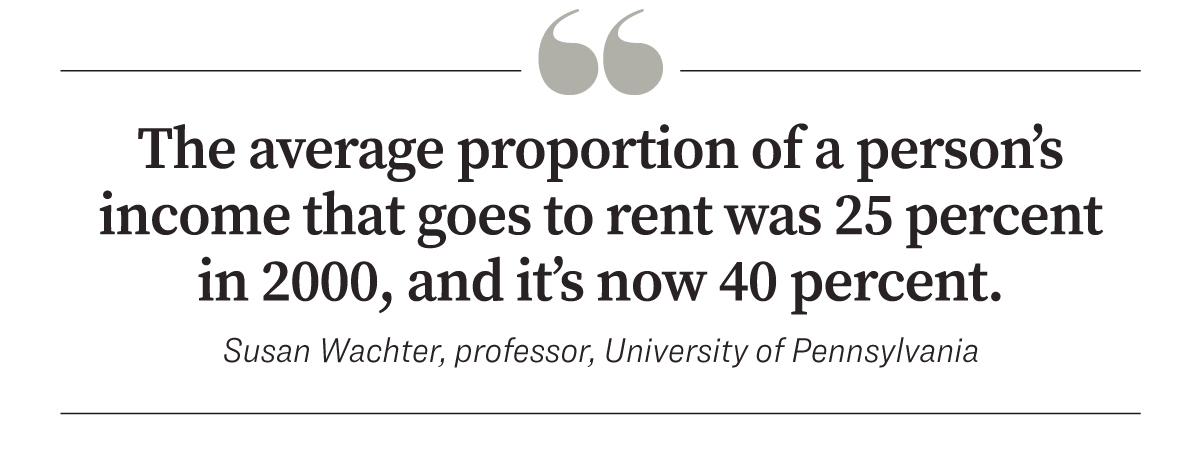

Yet for young Americans who can only afford to rent a home, more of their income is going toward rent than in years past. A study by Susan Wachter, professor of real estate and finance at the Wharton School of the University of Pennsylvania, found that 49 percent of those ages 18 to 29 chose to live with their parents in 2021 compared with a much lower 27 percent in 1960.

“The average proportion of a person’s income that goes to rent was 25 percent in 2000, and it’s now 40 percent. That’s really a striking increase,” Ms. Wachter said in a statement.

While year-over-year wages grew considerably after the COVID-19 pandemic for those younger than 40, data from the Federal Reserve Bank of Atlanta show that wage growth peaked in 2022 before falling each subsequent year as median home prices continued their ascent.

Unemployment rates also ballooned during the COVID-19 pandemic, rising to 14.8 percent in April 2020. The rate plunged as the economy slowly recovered, dropping to 3.4 percent in 2023, but it rose to 4 percent in May.

A sign advertising units for rent is displayed outside a building in New York City on April 11, 2024. (Spencer Platt/Getty Images)

Debt and Spending Habits

For study findings published by LendingTree on June 24, researchers analyzed more than 428,000 anonymized credit reports from users in the 100 largest U.S. metropolitan areas.It found that in those areas, 97.1 percent of Gen Zers possess non-mortgage debt of some kind and that Gen Z is the most likely age group to have this type of debt. Among them, roughly 80.8 percent have credit card debt, and the median non-mortgage debt for that age group hovers at about $16,562.

As a group, millennials owe even more. Their non-mortgage debt averages $30,558, and 38.4 percent of them have student loan debt, which is the highest for any age group. Millennials are also the second most likely age group to have personal loans, with 16.8 percent owing a median balance of $2,921.

A 2023 report from the surveying company Morning Consult found that millennials and Gen Z adults were spending more than $400 monthly on travel, recreation, and dining out in July of that year.

Looking nationwide, that report found 42.6 percent of millennials and 33.2 percent of Gen Z adults reported having credit card debt in August 2023.

Housing market expert Sofia Vyshnevska, chief operating officer and co-founder of NewHomesMate, a new-construction housing marketplace, said that the millennial and Gen Z debt-to-income ratios can be “heavily impacted by student loans,” making it harder to qualify for lending.

“Even those lucky enough not to have student debt are pushing their homeownership plans to around age 30,” she told The Epoch Times.

One reason is a “significant housing shortage” of approximately 3.2 million homes, and another is the meteoric rise in home values, she said.

Some, however, disagree that debt and spending habits are the main factors holding back millennials and Gen Zers from owning homes; Ms. Douglass calls it a “dangerous” stereotype.

She said credit card debt “definitely comes into play” when you’re trying to qualify for a mortgage, but she questions whether younger people spend more in general.

For those younger than 40, Ms. Modares said, spending is more about the “cost of living versus wages.”

The cost of housing rose by 5.4 percent from May 2023 to May 2024 alone, according to the U.S. Bureau of Labor Statistics. Transportation costs increased by 10.5 percent, and electricity increased by 5.9 percent.

For Gen Zers such as Harrison, debt isn’t a consideration. At 27, he has no student loan or credit card debt and has paid off his car. Even with $30,000 in savings, he’s unsure if he will ever own the modest house of his dreams.

People dine at a restaurant at Hudson Yards in New York City on Feb. 12, 2021. (Angela Weiss/AFP via Getty Images)

The Path to Homeownership

Given all of the factors impeding young people from becoming homeowners, it’s not always clear how to overcome those odds.Ms. Vyshnevska, who is in the new-construction business, said one option is to look for new-construction financing incentives.

“Many builders are offering interest-rate buydown programs, down payment assistance, free upgrades, and some go even as far as eliminating closing fees,” she said. “This definitely helps to decrease the burden and make homeownership more affordable.”

For entrepreneurs such as Mr. McDonald, one solution is to find a passive income stream. Another option is to find a business partner, whether a friend or significant other, and pool together resources to buy a house.

With two incomes and two sources of credit, an expensive property for a single person could become attainable for two. However, he said, it’s important to consult a lawyer before such a sale to have any necessary legal contracts or documents drafted to cover future changes, such as one buyer wanting to sell in five years against the wishes of the other.

Ms. Douglass and Ms. Modares took a similar approach before they started their real estate business in Austin. They also saw a gap in educational outreach for first-time buyers.

“And specifically, for first-time buyers wanting to do things in a different way—to do things creatively, to do things outside of the traditional way, that’s, you know, you get married, have a kid, then buy a house,” Ms. Douglass said.

Despite the roadblocks that young people face when thinking about the looming prospect of homeownership, Ms. Modares insists that the dream “is still possible.”

She tells first-time buyers, “There’s still hope,” especially if they see it as an investment toward a better home in the future.

Ms. Douglass offers them another perspective: that they can keep renting, but if they choose to buy, they can supplement a mortgage by renting out rooms.

“Then from there, you can figure out your strategy,“ she said. ”Maybe you just buy one house, and you house-hack it so that you’re paying very little.

“If we can look at it more of like a tool in your finances, there’s so much power there that you have access to when you own a home.”

Ms. Vyshnevska said purchasing a first home might be challenging, but she tells young buyers not to give up.

“Believe in your dreams, be patient, and don’t be discouraged by obstacles,” she said.

Naveen Athrappully contributed to this report.